Opening a dedicated IBAN in Europe is often a major challenge for high-risk businesses. Traditional banks tend to refuse these clients, citing regulatory exposure, compliance costs, and reputational risks. As a result, many legitimate companies — from crypto projects to gaming, fintech, or nutraceuticals — find themselves unable to access basic banking services. LegalBison. According to Eurochambres, regulatory barriers to bank accounts continue to slow down SMEs across Europe. Eurochambers.

Traditional banks decline high-risk clients primarily due to regulatory requirements, the cost of risk management, and the potential for financial loss. Here's a breakdown of the key reasons: * **Regulatory Compliance (KYC/AML):** Banks are heavily regulated to prevent money laundering (AML) and ensure they know their customers (KYC). High-risk clients often involve more complex due diligence, making compliance more resource-intensive and potentially increasing the bank's exposure to regulatory penalties if not handled perfectly. * **Credit Risk:** High-risk clients inherently have a higher probability of defaulting on loans or other financial obligations. Banks are in the business of lending money and need to ensure they can recoup their investments. Accepting too many high-risk clients significantly increases the chance of loan losses, which can impact the bank's profitability and solvency. * **Reputational Risk:** Associating with certain high-risk industries or individuals can damage a bank's reputation. This can lead to a loss of confidence from other customers, investors, and regulatory bodies, ultimately affecting business. * **Operational Costs:** Managing high-risk clients often requires more specialized staff, more extensive monitoring, and more complex security measures. These increased operational costs can make serving such clients less profitable, even if the initial transactions seem lucrative. * **Profitability vs. Risk Appetite:** Banks have a defined risk appetite, which is the level of risk they are willing to accept in pursuit of their business objectives. High-risk clients often fall outside this appetite because the potential rewards do not adequately compensate for the increased likelihood of financial distress or regulatory scrutiny. * **Capital Requirements:** Banks are required by regulators to hold a certain amount of capital against their assets, based on their riskiness. Higher-risk loans and clients require more capital to be set aside, which can tie up funds that could be used for more profitable, lower-risk ventures. * **Simplicity and Efficiency:** Traditional banking models are often built for efficiency and high volume. Processing a large number of standard transactions is more straightforward and cost-effective than dealing with complex, bespoke, or high-risk situations that require significant manual intervention and specialized analysis. While some "high-risk" clients might be perfectly legitimate businesses or individuals in industries that are simply perceived as riskier (like cannabis or certain online businesses), banks often err on the side of caution to protect their financial health and regulatory standing.

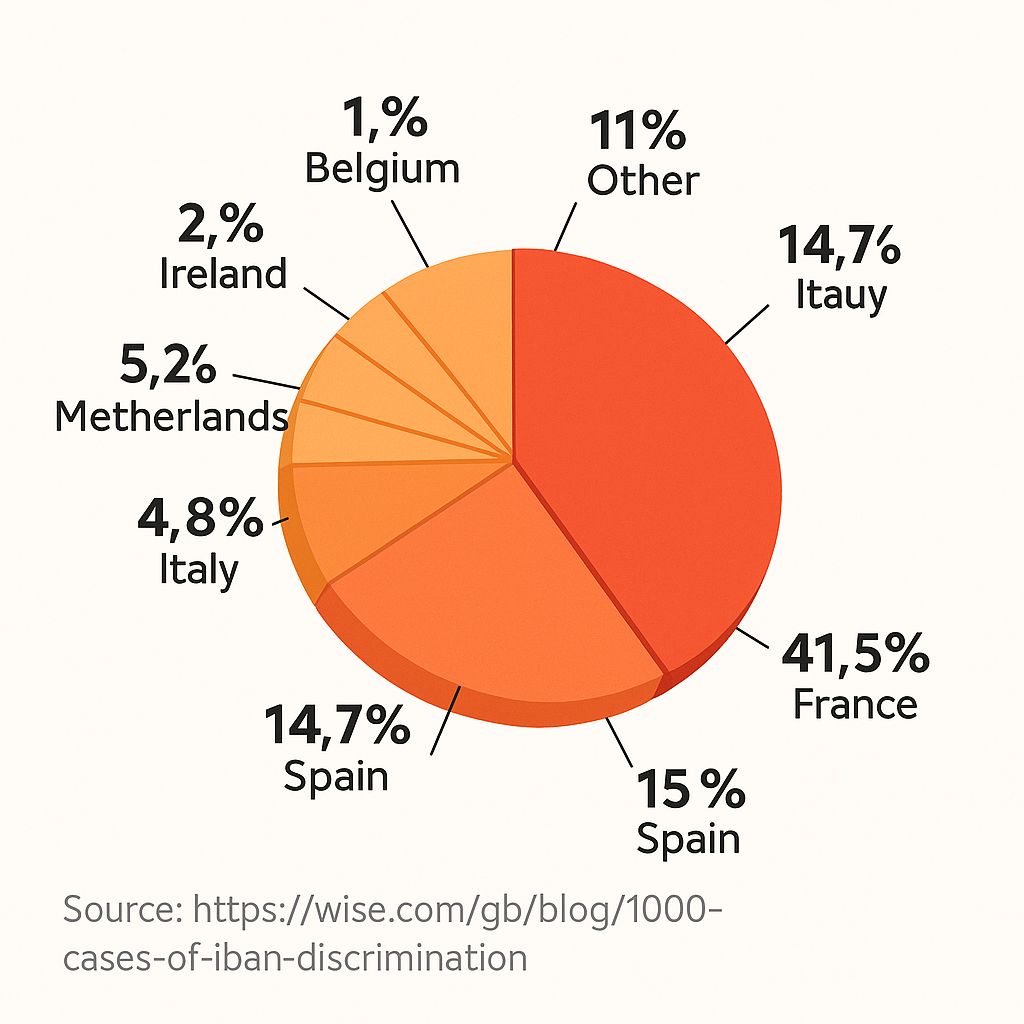

Banks in the EU operate under strict AML and MiCA regulations. High-risk industries are frequently perceived as too costly to monitor or too exposed to fraud. The result is “IBAN discrimination” — even businesses incorporated legally in the EU can face blocked or refused accounts. Between 2021 and 2023, over 3,500 such cases were reported in France and Spain alone. Euronews.

Geographic split in IBAN discrimination across Europe

Step 1: Prepare Documentation

Before applying for a dedicated IBAN account, businesses must prepare full KYC/KYB packages, including company incorporation documents, proof of funds, ultimate beneficial owner (UBO) declarations, and business activity details. Incomplete or inconsistent documentation is one of the main reasons for rejections.

Step 2: Choose a Risk-Friendly Provider

Instead of relying on legacy banks, many businesses turn to risk-friendly financial providers like Xpaid. As a licensed EMI, Xpaid offers dedicated IBAN accounts tailored to high-risk industries. The difference lies in the infrastructure: onboarding processes are transparent, risk models are adapted, and compliance teams understand the specifics of high-growth but risk-classified industries. This ensures businesses can operate within legal frameworks without facing unnecessary shutdowns.

Step 3: Open the Account and Integrate Stablecoins

Once approved, companies can access euro-denominated corporate IBANs. With Xpaid, this account can also integrate seamlessly with stablecoin on/off ramp infrastructure, allowing businesses to combine traditional banking rails with digital assets. This hybrid approach enables faster settlements, cross-border payments, and a smoother experience for international partners.

Banking Access Without Barriers

High-risk businesses deserve fair access to financial services. By offering dedicated IBANs that combine compliance, stability, and crypto integration, Xpaid provides a solution where traditional banks hesitate. For industries shut out by legacy banking, Xpaid ensures continuity, growth, and global reach.